Brent vs. WTI: Economic Growth's Role in Pricing

Brent vs. WTI: Economic Growth's Role in Pricing

Brent Crude and WTI are two key oil price benchmarks with distinct differences:

- Brent Crude: Sourced from the North Sea, used globally, easier to transport, and sensitive to international demand.

- WTI (West Texas Intermediate): Sourced from U.S. states like Texas, more tied to domestic U.S. markets, and known for higher quality (lighter and sweeter).

Key Points:

- Economic Growth Impact: Brent reacts more to global economic trends, while WTI is influenced by U.S. market conditions.

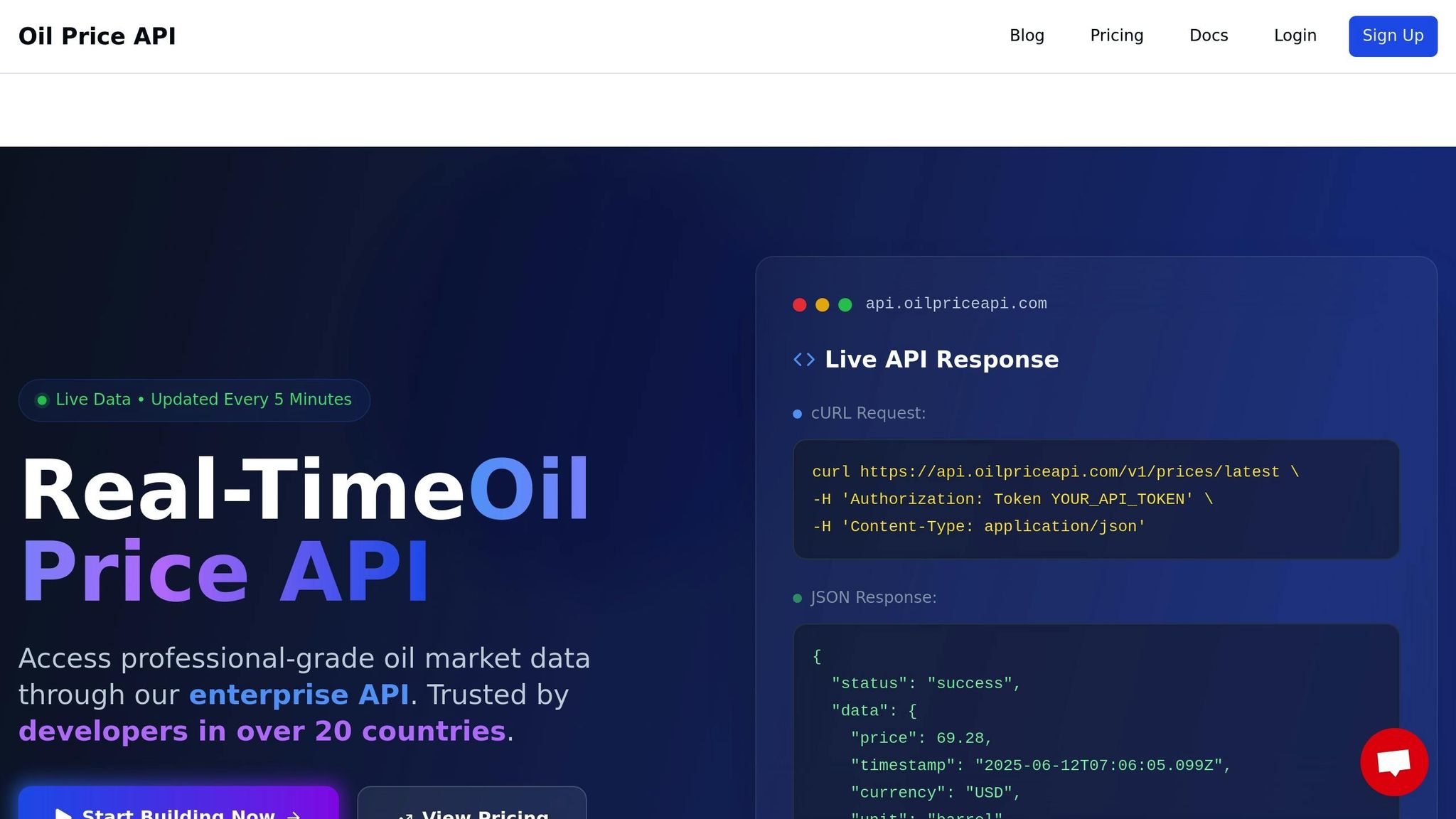

- Current Prices (June 12, 2025): Brent is priced at $69.45 per barrel, WTI at $67.91 per barrel.

- Demand Drivers: Emerging markets like China and India drive Brent demand, while U.S. refining activity shapes WTI pricing.

- Supply Factors: Brent benefits from offshore production; WTI relies on U.S. pipelines and exports.

Quick Comparison Table:

| Feature | Brent Crude | WTI Crude |

|---|---|---|

| Origin | North Sea | U.S. (Texas, North Dakota, Louisiana) |

| Market Sensitivity | Global | Domestic (U.S.) |

| API Gravity | 38° | 39.6° |

| Sulfur Content | 0.40% | 0.24% |

| Transportation | Offshore, easier shipping | Landlocked, pipeline-dependent |

| Current Price | $69.45 per barrel | $67.91 per barrel |

Economic growth drives oil demand, with Brent reflecting global trends and WTI tied to U.S. conditions. For traders and analysts, real-time data is essential to navigate these dynamics effectively.

Economic Growth and Global Oil Demand

GDP Growth and Oil Demand Connection

Economic growth and oil consumption often go hand in hand. As GDP increases, nations require more energy to fuel their industries, transportation systems, and expanding economies. This connection is especially noticeable in developing countries, where rapid industrialization drives up energy needs significantly.

Emerging economies are at the forefront of global oil demand growth. Projections indicate these markets will contribute an additional 860,000 barrels per day (bpd) in oil demand this year and 1 million bpd next year. In contrast, developed OECD nations are expected to see declines in oil demand, with reductions of 120,000 bpd in 2025 and 240,000 bpd in 2026.

Looking ahead, global oil demand growth is expected to slow. Forecasts suggest a decrease from 990,000 bpd in early 2025 to 650,000 bpd later in the year, averaging about 750,000 bpd during 2025–2026.

Goldman Sachs Research anticipates that energy needs in emerging markets will rise sharply, fueled by GDP growth of nearly 4% annually in the latter half of this decade. As Daan Struyven, co-head of Global Commodities Research at Goldman Sachs, explains:

"Looking further, we expect oil demand to grow for another decade."

These trends underscore how the economic trajectories of emerging markets are shaping the future of global oil demand.

Emerging Markets Drive Oil Demand

In 2024, about three-fourths of global oil consumption growth is expected to come from five countries: Brazil, China, India, Indonesia, and Saudi Arabia. These economies not only consume more oil but also influence global pricing dynamics for benchmarks like Brent and WTI.

China and India stand out as major drivers. China’s growing petrochemical sector and India’s clean cooking initiatives are expected to boost demand for products like LPG, ethane, and naphtha. According to the IEA, emerging Asian economies could consume approximately 600,000 bpd more oil in 2026 compared to 2025, while OECD nations are projected to see a year-over-year decline in demand.

Economic fluctuations also play a role in demand shifts. For instance, in March 2025, India’s oil demand dropped for the second consecutive month, declining by 20,000 bpd year-over-year, while Brazil’s consumption exceeded expectations. Trade tensions add further complexity, with the IEA revising its 2025 global GDP growth forecast from 3.1% to 2.4%. This adjustment could disproportionately affect oil-dependent developing economies. Analysts at S&P Global Commodity Insights suggest that if global GDP growth slows to 1.6% in 2025, oil demand growth could shrink from 1.2 million bpd to as low as 700,000 bpd.

The impact on pricing varies by benchmark. Brent crude, with its waterborne supply, is more sensitive to global demand, particularly from Asia and the Middle East, as its transportation to distant markets is relatively straightforward. On the other hand, WTI prices are largely shaped by U.S. market conditions due to its landlocked supply and infrastructure.

Forecasts for oil demand growth vary. The IEA predicts an increase of about 730,000 bpd this year, while OPEC anticipates growth of 1.3 million bpd in both 2025 and 2026. As Haitham Al Ghais, OPEC Secretary-General, puts it:

"There is no peak in oil demand on the horizon"

OPEC’s optimism reflects confidence in the sustained growth of emerging markets. Industrialization and a growing middle class in these regions are expected to drive higher energy and transportation needs, further influencing global oil demand and pricing dynamics for benchmarks like Brent and WTI.

Supply and Demand: Brent vs. WTI

Supply Factors for Brent and WTI

The supply dynamics of Brent and WTI are shaped by their distinct origins and infrastructure. WTI, predominantly sourced from the U.S., owes much of its production to the Permian Basin, which hit a record 5.9 million barrels per day in April 2025. Meanwhile, Brent crude, extracted from the North Sea, has seen production decline from about 850,000 barrels per day to under 700,000 barrels per day since late 2020.

Brent's sea-based production offers a cost advantage in transportation, while WTI's inland production has historically faced higher logistical costs. This difference makes Brent more responsive to global demand shifts tied to economic growth, whereas WTI has traditionally been more influenced by U.S. market conditions. However, changes in U.S. export policies have altered WTI's role in the global market. Crude oil exports from the U.S. surged from 400,000 barrels per day in 2015 to over 4 million barrels per day. As Vera Blei from S&P Global Platts notes:

"Since the restart of U.S. crude exports in 2015, WTI Midland has become a baseload grade for European refiners and a core part of the North Sea oil market."

While U.S. shale oil production shows signs of plateauing, global supply is further shaped by OPEC+ decisions on production levels. The group faces pressure to reassess earlier production cuts. Overall, global oil supply is expected to rise by 1.6 million barrels per day, averaging 104.6 million barrels per day in 2025.

These supply contrasts underscore how regional differences influence the demand for Brent and WTI.

Demand Influences on Brent and WTI

While supply factors establish baseline differences, regional demand adds another layer to the pricing gap between Brent and WTI. Brent serves as the global benchmark, pricing about two-thirds of the world’s internationally traded crude oil. This makes Brent highly sensitive to worldwide economic trends and shifts in international demand. On the other hand, WTI’s demand is more closely tied to U.S. market dynamics. For example, in 2023, the U.S. consumed 20.25 million barrels per day while producing approximately 21.91 million barrels per day, accounting for over 22% of the world’s oil supply. In comparison, Saudi Arabia and Russia each contributed about 11%.

Regional demand imbalances directly affect the price disparity between the two. As of May 2025, WTI traded at $57.16 per barrel with a slight 0.05% increase, while Brent declined by 1.73% to $60.23. WTI benefits from strong U.S. refining activity, while Brent faces challenges from weaker demand in European and Asian markets.

Shifts in global oil trade and U.S. export trends have also influenced demand dynamics. For instance, U.S. crude exports to Europe exceeded 1 million barrels per day in March, reaching as high as 1.25 million barrels per day. This has made Brent more sensitive to U.S. market factors. Rebecca Babin, senior energy trader at IBC Private Wealth US, explains:

"Bottom line for Brent is that it will be much more influenced by U.S. fundamentals such as Strategic Petroleum Reserve releases and Permian production."

Market sentiment has also shifted. Hedge funds have reduced long positions by 14% in the past month, reflecting increased bearishness. Meanwhile, financial institutions like Morgan Stanley and Goldman Sachs have lowered their forecasts, citing concerns over oversupply and uncertain demand.

How Economic Growth Affects Brent vs. WTI Pricing

Global vs. Regional Demand Effects

Economic growth plays a key role in shaping the pricing of Brent and WTI crude oil, further highlighting the differences between these two benchmarks. Brent, with its international reach, is particularly sensitive to global economic trends.

For instance, when emerging markets undergo rapid industrial growth, Brent tends to react more significantly than WTI. Take China's recent economic activity: in April 2025, industrial production grew by 6.1% year-over-year, and retail sales rose by 5.1%. These developments directly affect Brent pricing, as demand from emerging markets exerts a stronger pull on Brent compared to WTI. As a Bloomberg analyst notes:

"Brent represents the Northwest Europe sweet market, but since it's used as the benchmark for all West African and Mediterranean crude, and now for some Southeast Asia crudes, it's directly linked to a larger market."

On the other hand, WTI pricing is shaped more by domestic U.S. factors. It reflects supply and demand dynamics within the U.S. market. For example, when the Permian Basin hit a record output of 5.9 million barrels per day in April 2025, the resulting supply surge had a more pronounced effect on WTI prices than on Brent. This contrast underscores how economic growth impacts these benchmarks differently.

Currently, the price gap between the two benchmarks stands at $3.61 per barrel. As of April 30, 2025, WTI crude traded at $60.34 per barrel, while Brent crude was priced at $63.95 per barrel. This spread fluctuates depending on how global versus regional economic trends influence each market.

Brent vs. WTI Pricing Factors Table

The table below summarizes the key pricing factors shaped by economic growth:

| Factor | Brent Crude | WTI |

|---|---|---|

| Market Sensitivity | Global economic conditions across Europe, Asia, and Africa | U.S. domestic economic indicators and regional demand |

| Economic Growth Impact | Reacts to industrial growth in emerging markets, especially in China and Southeast Asia | Driven by U.S. manufacturing, refinery activity, and domestic consumption |

| Geopolitical Influence | Highly sensitive to OPEC+ decisions and Middle East tensions | Less affected by global conflicts, more influenced by U.S. energy policy |

| Supply Chain Factors | Offshore production supports efficient international shipping | Pipeline-reliant distribution impacts regional pricing |

| Oil Quality | API gravity of 38.06, sulfur content 0.37% – suitable for diverse products like diesel | API gravity of 39.6, sulfur content 0.24% – ideal for gasoline production |

| Trade Exposure | Prices two-thirds of globally traded oil contracts | Primarily serves as a reference for the U.S. market |

This table highlights Brent's greater sensitivity to global factors, while WTI remains more closely tied to domestic influences. For example, during periods of global uncertainty, Brent prices often experience more pronounced volatility due to its broader international exposure.

Regional infrastructure also plays a key role in how economic growth translates into pricing. Brent's offshore production allows for efficient transport to global markets, making it more responsive to growth in regions with strong maritime trade. In contrast, WTI's reliance on pipelines and storage facilities makes it more attuned to activity within North America's energy networks. These logistical differences further contribute to how economic trends uniquely affect each benchmark.

sbb-itb-a92d0a3

Real-Time Price Monitoring and Analysis

Why Data Matters in Oil Price Analysis

Having accurate, real-time market data is essential for understanding how economic growth influences Brent and WTI oil prices. The oil market moves fast, and delays in accessing updated information can lead to missed opportunities. Moody Sultan, Product Manager at Sparta, highlights this point:

"The days when traders could effectively operate with delayed pricing are firmly in the past. Trading without access to real-time pricing is not just inefficient, but a fundamental disadvantage for oil market participants in today's environment."

For instance, on June 12, 2025, Brent Crude was priced at $69.45 per barrel, while WTI stood at $67.91 per barrel. These figures are constantly shifting, influenced by factors like economic indicators, supply chain disruptions, and changes in demand. Real-time data allows traders to stay updated on critical market elements such as prices, weather conditions, and grid statuses, enabling quick decision-making. This is particularly crucial in understanding how rapid industrial growth in emerging economies like China and India drives increased energy consumption.

Historical data is equally important. Analysts use it to detect structural changes in the WTI-Brent price spread, such as the significant shift that occurred in January 2011. Advanced analytics tools help process both historical and real-time data, revealing patterns and generating actionable insights for traders looking to capitalize on short-term opportunities. In this fast-paced environment, having a dependable solution like OilpriceAPI is essential.

How OilpriceAPI Helps with Analysis

OilpriceAPI provides seamless access to real-time and historical price data for Brent Crude and WTI through its JSON REST API. This comprehensive data source empowers users to make well-informed decisions and adapt quickly to market changes. Moody Sultan underscores the importance of reliability in such a competitive space:

"In a market where seconds can be the difference between profit and loss, a unified, reliable source of truth provides a genuine competitive advantage."

The platform’s extensive historical data capabilities support long-term trend analysis, helping users identify patterns, anomalies, and opportunities through visualization tools. With its user-friendly API integration, OilpriceAPI caters to a range of needs - from individual trading strategies to enterprise-level market analysis. This versatility enables users to execute both short-term tactical moves and long-term strategic plans effectively. By offering both real-time updates and historical context, OilpriceAPI equips traders and analysts with the tools they need to understand and respond to the impact of economic growth on Brent and WTI pricing.

Brent-WTI Futures Spread | Why WTI price is lower then BRENT? | WTI Pricing Explained

Conclusion: Economic Growth's Role in Brent and WTI Pricing

Economic growth plays a critical role in shaping the prices of both Brent and WTI, though each reacts to different influences. Brent tends to mirror global economic shifts, while WTI is more attuned to regional factors within the U.S.

As of June 11, 2025, Brent was priced at $68.73 per barrel, while WTI stood at $65.99 per barrel, creating a spread of $2.74. This gap has widened compared to last year’s $1.59 spread. The difference highlights how distinct economic forces impact the pricing of these benchmarks.

Global factors, such as China’s 6.1% industrial growth, have a noticeable impact on Brent prices. Meanwhile, U.S.-specific production dynamics remain the primary driver for WTI pricing . These trends emphasize the importance of continuous and real-time market analysis.

Supply and demand fundamentals remain at the core of price movements. For instance, rising inventories could lead Brent prices to average $61 per barrel in 2025 and $59 in 2026, according to EIA forecasts. These numbers illustrate how broader economic conditions influence long-term price trajectories.

To navigate these complexities, market participants need reliable, up-to-date information. Tools like OilpriceAPI provide real-time updates every 5 minutes, coupled with extensive historical data for both Brent and WTI. This allows traders and analysts to closely monitor how economic developments affect pricing. With energy companies across more than 20 countries relying on such insights, the link between economic growth and oil pricing remains a cornerstone of the global energy market.

The interplay between global economic trends and regional production patterns underscores the ongoing importance of economic growth in shaping oil prices. As global energy dynamics continue to shift, staying informed through continuous monitoring will remain essential for anyone involved in the market.

FAQs

How do global economic trends affect Brent Crude prices compared to WTI?

Global economic trends significantly influence the prices of Brent Crude and WTI, primarily through the balance of supply and demand. Brent Crude, a key global benchmark, is particularly sensitive to international factors like economic growth, geopolitical developments, and shifts in worldwide energy demand. When the global economy experiences robust growth, demand for Brent tends to rise, pushing prices higher due to its accessibility in international markets.

In contrast, WTI pricing is more closely aligned with domestic factors in the United States. Elements such as local production levels, storage capacity, and transportation infrastructure play a major role. While WTI is not immune to global influences, its price often reflects U.S.-specific dynamics, like output from shale oil fields or pipeline limitations.

The difference in pricing between these two benchmarks, known as the Brent-WTI spread, highlights these distinctions. Brent usually trades at a premium, driven by its lower shipping costs and higher global demand. Grasping how these benchmarks react to economic changes is crucial for understanding crude oil markets and making sound decisions.

What drives the demand for Brent Crude in rapidly growing economies like China and India?

The appetite for Brent Crude in rapidly developing nations like China and India is closely tied to economic growth and industrial expansion. As these countries continue to grow, their energy requirements escalate to fuel infrastructure development, manufacturing, and the increasing consumption habits of a burgeoning middle class.

Take India, for instance. Its oil demand is expected to climb at an annual rate of 3.2% by 2025, significantly outpacing China's slower growth rate of 1.7% over the same timeframe. This surge in demand reflects India's heavy investments in energy-intensive sectors and urbanization efforts. On the other hand, while China has historically driven global oil demand, its growth has recently tapered off due to struggles in its property market and broader economic challenges. These trends underscore how deeply economic momentum impacts Brent Crude consumption in these influential markets.

How do U.S. market conditions uniquely affect WTI prices compared to Brent Crude?

WTI and Brent Crude prices are shaped by distinct market forces, largely due to their geographic origins and logistical setups. WTI, extracted from landlocked areas in the U.S., is strongly influenced by domestic factors such as production rates, consumption patterns, and transportation challenges. For instance, bottlenecks at critical hubs like Cushing, Oklahoma - where WTI futures are settled - can lead to noticeable price swings.

On the other hand, Brent Crude, sourced from offshore fields in the North Sea, benefits from easier access to global markets. This makes its price more sensitive to international supply and demand dynamics, as well as geopolitical events. While WTI prices are closely tied to U.S. economic activity and shale oil output, Brent is more impacted by global developments and decisions made by OPEC. These contrasts underscore how domestic conditions uniquely shape WTI pricing, setting it apart from the more globally influenced Brent.